Nestlé (NESN) is one of Europe’s most iconic companies — a centuries‑old food and beverage powerhouse recognized anywhere in the world. Who doesn’t appreciate a Nespresso coffee, Häagen-Dazs ice-cream or KitKat chocolate?

It’s also famous among investors for its reliable and steadily rising dividends.

But does that mean the stock is a wise investment today?

In this Nestlé stock analysis, we’ll break down the business using my simple, fundamentals‑driven stock analysis approach to find out whether it deserves a place in a long‑term, disciplined portfolio.

Let’s dive in.

Full disclosure: I don’t own Nestlé stocks at the time of writing this analysis.

⚡Key Takeaways

- Nestlé is a global food and beverage giant with iconic brands that everyone recognises.

- Despite its reputation and dividend track record, the company has stopped growing.

- Debt‑to‑equity ratio has deteriorated sharply, rising from 40% (2018) to 134% (2025).

- Fair value estimate suggests the stock is overvalued by 64–73%.

- Final take on Nestlé: too expensive! It’s a reliable dividend payer but that alone doesn’t justify overpaying.

What Does Nestlé Do?

Nestlé is a well-known Switzerland-based food and beverage company that most of us welcome in our home.

The company’s product categories include powdered and liquid beverages, water, milk products and ice cream, nutrition and health science, prepared dishes and cooking aids, confectionery, and pet care.

Its portfolio includes brands such as Nescafé and Nespresso coffee, S.Pellegrino water, Häagen-Dazs ice-cream, KitKat and Smarties chocolate, Friskies and Purina pet food.

Nestlé is also known for its early childhood and family nutrition products. Plus, it owns many local brands all over the world.

Stock Price Long‑Term Trend

Nestlé’s long-term stock price chart shows 40+ years of steady growth. However, the stock peaked in early-2022 and has since crashed back to 2018 price levels where it stands today.

This makes me question: what happened during the last 8 years that caused the stock to stagnate?

We need to look into the business financials and follow its earnings past performance to find the answer.

Nestlé Fundamental Analysis

Let’s explore the fundamentals of Nestlé then.

1. Past Performance

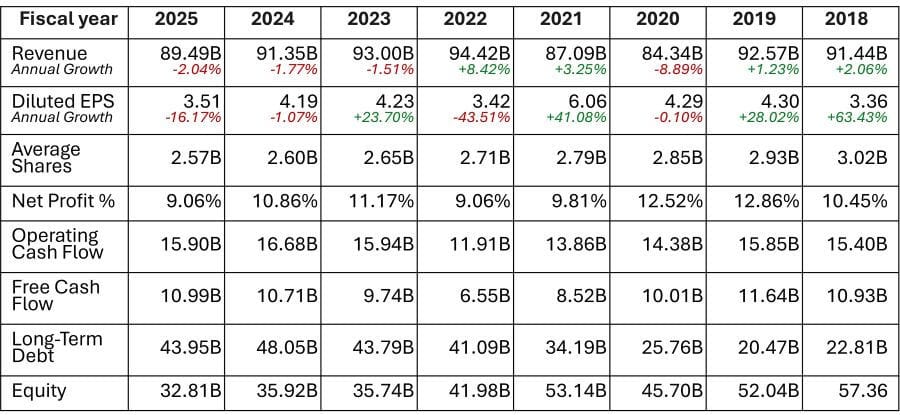

Revenue

Revenue went nowhere really between 2018 and 2025, just circling around CHF 90 B. There’s not even keep-up-with-inflation growth here.

Earnings

Nestlé’s earnings per share show a similar performance although with far more volatility over the same period. They peaked at CHF 6.06 in 2021 before being dragged back to CHF 3.50-4.30 range again like gravity force.

Share Count

The number of shares outstanding in the market has been reduced by around 15%, from 3.02B to 2.57B. But buybacks didn’t meaningfully boost the company’s earnings per share because earnings didn’t grow.

Net Profit Margin

Net profit margins have been stably hovering around 10–12% between 2018 and 2025. That’s not too bad, but not much of a brand pricing power also.

Cash Flow

Both operating and free cash flow are positive but hardly moved over the years. Unsurprisingly there isn’t any growth here either.

2. Financial Health

The company’s financial position is deteriorating.

2025’s debt-to-equity ratio of 134% is quite high. And has been getting worse over time. In 2018, deb-to-equity ratio was just 40%. This is a red flag.

I prefer companies with low and stable debt, ideally under 30%.

3. Dividends

Nestlé pays a forward dividend of CHF 3.10 per share, yielding a notable 4.1%. And it has delivered a consistent and increasing dividend for more than twenty years.

4. Growth Outlook

Past Growth

As we’ve seen the company is not growing in any way. Neither revenue, earnings or cash flow show any sign of moving up or down.

Future Expectations

Time to move on to my educated guesstimate on Nestlé based on past performance.

There’s not much to work with here to be honest. The company’s reputation and brands are hugely recognized and respected. But it clearly is missing a path to expand further.

For that reason, the best that I can expect is a 2-4% annual earnings growth over the coming years. That’s just to keep up with inflation. And that puts Nestlé in the “slow grower” category.

Nestlé Fair Value Estimate

Now let’s run our back-of-the-envelope valuation assessment. The goal is to get an approximation interval through quick and simple calculations.

Owner’s Earnings

First, we estimate the total potential return on investment by using the owner’s earnings. This is nothing more than adding the expected future growth of earnings per share and the forward dividend yield.

Expected return = future EPS growth (2–4%) + dividend yield (4.1%) ≈ 6–8% per year

If the stock is fairly priced, this is the return an investor might expect.

PEG Ratio

Next, let’s assess whether the stock is trading at a fair price or not using the PEG ratio.

When we compare the current P/E ratio (TTM) of 22x with our owner’s earnings estimate of 6–8% it immediately screams overpriced.

PEG = P/E ÷ Owner’s earnings = 3.6 to 2.7

From the growth at a reasonable price approach, we know that a PEG above 1 suggests overvaluation. And a PEG above 2 suggests the stock is way too expensive for the return it offers.

Fair Value Estimate

If Nestlé was priced in line with its growth (PEG ≈ 1), its P/E should be between 6–8x versus today’s 22x.

This implies the stock currently trades at a premium of 64–73% versus our fair value estimate.

Conclusion: Is Nestlé a Good Investment?

Here’s my final take on Nestlé: a European giant in food and beverage products but unfortunately, it’s way too expensive.

Why? Let’s recap everything.

Does the Company Have Solid Financials?

Not really. Nestlé is a profitable and cash positive company, stable but without growth. Sadly, it has high and ever-increasing levels of debt that risk its future and dividend paying track record.

Do I Understand the Business Model?

Yes. The company holds many of the brands that we know and love for many years. They’re in the shelf of every supermarket we go and every house we visit.

Consumer preferences change over time, but it’s hard to imagine a future without Nestlé and its most iconic products.

Does It Trade at a Fair Price?

No. Based on this simple stock analysis approach, we can clearly say that Nestlé is way overpriced relative to its expected growth. The stock trades at a premium of 64–73% versus our fair value estimate.

👉 Action step: Take another look at Nestlé using your own assumptions. Do you agree with this assessment, or do you see something I’ve missed? Share your thoughts in the comments — I’d love to hear your perspective.

And if you haven’t yet, subscribe for more fundamentals‑driven stock analyses.