L’Oréal (OR) is the largest beauty company in the world and holds a diverse brand portfolio covering skin and hair care, makeup, perfumes, and more. Its memorable slogan “Because You’re Worth It” has been around for more than 50 years.

The company is also a solid dividend payer too.

But is that enough to make it a wise investment today?

In this L’Oréal stock analysis, we’ll break down the business using my simple, fundamentals‑driven stock analysis approach to find out whether it deserves a place in a long‑term, disciplined portfolio.

Let’s dive in.

Full disclosure: I don’t own L’Oréal stocks at the time of writing this analysis.

⚡Key Takeaways

- L’Oréal is the largest beauty company in the world, with a globally dominant brand portfolio.

- The business shows solid fundamentals: steady revenue growth, strong cash flows, and low debt.

- Fair value estimate suggests overvaluation with the stock trading at a 64–77% premium.

- Final take on L’Oréal: too expensive! It’s a great business but there’s no way it justifies today’s price.

What Does L’Oréal Do?

L’Oréal is a France-based company that manufactures and sells cosmetic products worldwide.

It offers skin care products, makeup products, hair care products, perfumes, colouring products and others. Brand portfolio includes L’Oréal Paris, Garnier, Maybelline New York, NYX Professional Makeup, Lancôme, Vichy, and other brand names.

The company sells its products through multiple channels, such as hair salons, e-commerce, mass market retail, department store perfumeries, and pharmacies.

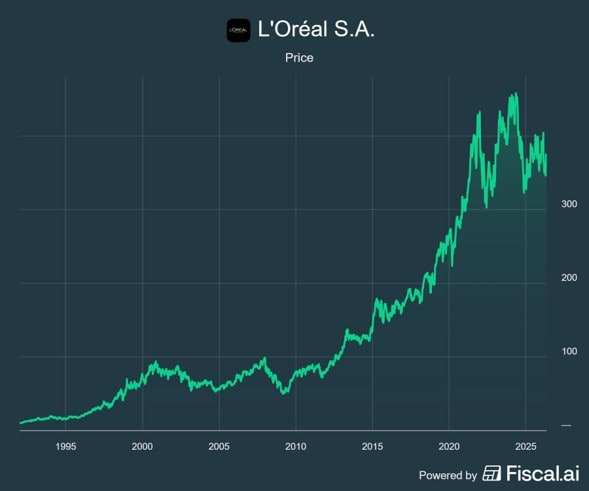

Stock Price Long‑Term Trend

L’Oréal’s long-term stock price chart shows 30+ years of steady compounding. However, over the last 5 years, the stock has mostly moved sideways, peaking in late-2021, mid-2022, and again in early-2024.

So, what’s the story behind this recent price lack of growth?

We’ll look into the business financials and follow its earnings past performance to find the answer.

L’Oréal Fundamental Analysis

Let’s explore the fundamentals of L’Oréal then.

1. Past Performance

Revenue

Revenue nearly doubled between 2018 and 2025, increasing from € 26.94 B to € 44.05 B — that’s roughly a 9% yearly growth on average. However, growth has slowed since 2023, suggesting the business may be entering a more mature phase.

Earnings

L’Oréal’s earnings per share behaved in a similar way although with added volatility. Again, we see yearly growth around 9% per year.

Share Count

The number of shares outstanding in the market has been reduced by around 5%, from 563.10 M to 535.37 M. But buybacks didn’t meaningfully boost the company’s earnings per share — see how profit growth and earnings per share growth are the same.

Net Profit Margin

Net profit margins have been quite stable and hovering around 14% during this period. That’s not bad for a consumer goods business but it also doesn’t scream exceptional pricing power.

Cash Flow

Both operating and free cash flow show a clear upward trend, having nearly doubled from 2018 to 2025.

L’Oréal clearly knows how to make money out of its brands and build a strong cash position over time.

2. Financial Health

The company is in a strong financial position.

The 2025 debt-to-equity ratio is well below the 30% ideal threshold. Plus, it’s been improving since long-term debt has been well under control while shareholders’ equity kept growing.

This gives L’Oréal flexibility during downturns and room to reinvest.

3. Dividends

L’Oréal pays a forward dividend of €7.20 per share, yielding a notable 2.1%. And it has delivered a consistent and increasing dividend for more than twenty-five years, making it a reliable income payer.

4. Growth Outlook

Past Growth

We’ve seen that both revenues and earnings per share increased around 9% annually from 2018 to 2025, though growth appears to be slowing down more recently. Also, growth was somewhat inconsistent year-over-year.

Future Expectations

Time to move on to my educated guesstimate on L’Oréal based on past performance.

The company’s leading market position should prevail over the long term, even if momentum shows early signs of a slowdown. Plus, there is enough cash flow to sustain though times, reinvest in the business, or pay higher dividends.

For that reason, I would expect a conservative 5-9% annual earnings growth over the coming years. That puts the company in between the “slow grower” and “stalwart” categories.

L’Oréal Fair Value Estimate

Now let’s run our back-of-the-envelope valuation assessment. The goal is to get an approximation interval through quick and simple calculations.

Owner’s Earnings

First, we estimate the total potential return on investment by using the owner’s earnings. This is nothing more than adding the expected future growth of earnings per share and the forward dividend yield.

Expected return = future EPS growth (5–9%) + dividend yield (2.1%) ≈ 7–11% per year

If the stock is fairly priced, this is the return an investor might expect.

PEG Ratio

Next, let’s assess whether the stock is trading at a fair price or not using the PEG ratio.

When we compare the current P/E ratio (TTM) of 31x with our owner’s earnings estimate of 7–11% we can see instantly that we are in overpriced territory.

PEG = P/E ÷ Owner’s earnings = 2.8 to 4.4

From the growth at a reasonable price approach, we know that a PEG above 1 suggests overvaluation. And a PEG above 2 suggests the stock is way too expensive for the return it offers.

Fair Value Estimate

If L’Oréal was priced in line with its growth (PEG ≈ 1), its P/E should be between 7–11x versus today’s 31x.

This implies the stock currently trades at a premium of 64–77% versus our fair value estimate.

Conclusion: Is L’Oréal a Good Investment?

Here’s my final take on L’Oréal: the world’s largest beauty company and a solid dividend payer but unfortunately, it’s way too expensive.

Why? Let’s recap everything.

Does the Company Have Solid Financials?

Yes. L’Oréal is a revenue and profit growing company even if they’re inconsistent and slowing down. It generates positive and growing cash flows that lead to a strong cash position and low levels of debt.

Do I Understand the Business Model?

Yes. The beauty industry is something we all have high exposure to daily. L’Oréal famous products are recognized and sold worldwide making it a very resilient business.

It seems fair to assume that the company won’t give up its dominant position anytime soon.

Does It Trade at a Fair Price?

No. Based on this simple stock analysis approach, we can clearly say that L’Oréal is way overpriced relative to its expected growth. The stock trades at a premium of 64–77% versus our fair value estimate.

👉Action step: Take another look at L’Oréal using your own assumptions. Do you agree with this assessment, or do you see something I’ve missed? Share your thoughts in the comments — I’d love to hear your perspective.

And if you haven’t yet, subscribe for more fundamentals‑driven stock analyses.